Weaponising the Balance Sheet: Why the FRS 102 Transition is No Longer Just a Compliance Exercise

The implementation of the revised FRS 102 lease accounting rules in January 2026 marked a permanent shift in UK corporate reporting. Yet, as businesses navigate the ongoing reality of these regulations, the true nature of the challenge is becoming clear. This was never a simple administrative box to tick; it is a complex, continuous process that is fundamentally changing how corporate agility is evaluated.

The legislation is now being utilised by the market in an entirely unforeseen way. It has evolved from a backward-looking statutory filing requirement into a live, public diagnostic tool used to audit your operational efficiency.

The Hidden Cost of Visibility

Commercial property is almost universally an organisation’s second-largest fixed cost, outstripped only by payroll. Historically, the true efficiency of this spend was safely obscured, tucked away in the extensive disclosure notes of financial accounts. Operating leases allowed companies to maintain expansive, sometimes inefficient physical footprints without altering the primary structure of their balance sheets.

Under the new rules, that protective veil has been entirely dismantled. Every commercial lease now sits squarely on the primary financial statements as a Right-of-Use asset matched by a lease liability.

The immediate consequence of this sudden transparency is sharp: your property portfolio is now entirely benchmarkable.

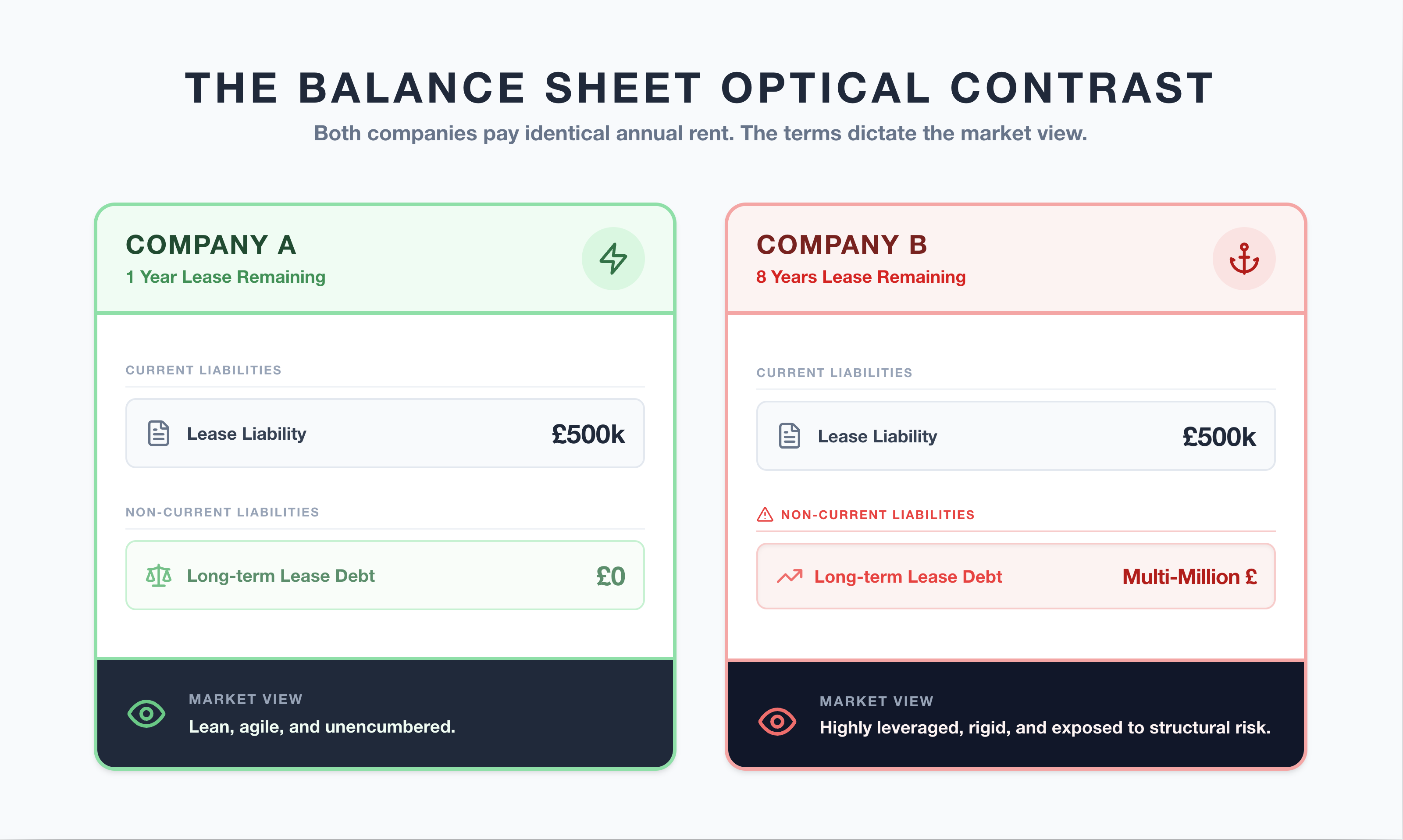

The Gearing Illusion: A Tale of Two Leases

To understand how this transparency surfaces perceived financial mismanagement, consider a simple scenario.

Company A and Company B are direct competitors with identical revenues. Both occupy similar office spaces and pay an identical rent of £500,000 per year. However, Company A has only one year remaining on their lease, while Company B is locked into an eight-year commitment.

Before January 2026, their primary financial statements looked identical. Today, Company B’s balance sheet will look vastly more debt-heavy.

Because FRS 102 requires the lease liability to be calculated on the net present value of all future commitments, Company B must report millions of pounds in long-term liabilities. The face of the balance sheet does not explain the lease length or the operational context; it simply displays the massive debt weight.

The Stakeholder Ecosystem: Who is Looking and Why It Matters

This balance sheet distortion carries immediate, real-world consequences. Your numbers are actively analysed by a broad ecosystem of external stakeholders, each viewing your lease liabilities through their own lens of risk, reward, and capability:

- Direct Competitors and Industry Peers: Competitors will use your raw lease liability figures to benchmark their own operational footprint against yours, instantly exposing any capital inefficiencies, wasted space, or bloated overheads to the wider market.

- Commercial Lenders and Banks: Lenders assess leverage to calculate borrowing capacity. A balance sheet artificially inflated by long-term, unoptimised lease liabilities alters your gearing ratios, which can inadvertently risk breaching debt covenants or heavily increase the interest rates on future credit lines.

- Institutional Investors and Shareholders: Equity markets look at Return on Capital Employed (ROCE). If your balance sheet carries heavy property liabilities that are not generating clear, matching returns, investors read it as poor capital allocation and a sign of operational bloat, downwards-adjusting their valuation of your business.

- Credit Rating Agencies: These agencies evaluate a business’s structural rigidity. A massive, inflexible long-term lease liability signals a high fixed-cost base that cannot be easily contracted during an economic downturn, lowering your corporate credit score.

- M&A Suitors and Acquirers: During corporate acquisitions, buyers look for hidden toxic drag. A legacy of poorly managed property commitments sitting permanently on the balance sheet is viewed as a structural liability that directly reduces the final purchase price.

- Enterprise Procurement Partners: Major corporate clients evaluating long-term supply chain stability run deep financial health checks on potential vendors. Appearing overleveraged due to unmanaged property commitments can see your business quietly dropped from major commercial tenders.

The Break Option Trap

This stakeholder scrutiny is compounded by how break options are handled. Under the regulations, a break option only reduces your balance sheet liability if management can prove to auditors that they are "reasonably certain" to exercise it.

If a company lacks centralised, defensible portfolio data, auditors will default to the most conservative approach: forcing the business to model the full, un-broken lease term. Overnight, a flexible 10-year lease with a Year 5 break is treated as a full decade of debt. The legal right to walk away remains hidden in the background, while the bloated liability remains on public display as a perceived metric of capital inefficiency.

Left unmanaged, these unwanted liabilities sit on the balance sheet for years, signalling a lack of proactive estate oversight and actively damaging your corporate reputation.

Shifting from Compliance to Strategic Defence

When the stakes are this high, treating lease accounting as a temporary hurdle is a major oversight. Managing this is a significant, ongoing operational process. The primary objective for corporate leadership today is to ensure that mandatory compliance does not inadvertently broadcast operational weaknesses to the market.

This is exactly where Leamur changes the equation.

We provide the modern data infrastructure required to move from reactive reporting to a proactive strategic defence. Leamur centralises and clarifies portfolio data, giving finance and property executives the exact insights needed to optimise lease terms, validate strategic intent to auditors, and ensure that toxic, non-performing property commitments do not linger on the balance sheet.

The new era of lease accounting isn't about satisfying a regulatory mandate—it's about protecting your market position. With Leamur, you can ensure that your financial statements reflect calculated operational strength, not unmanaged corporate liabilities.